Share:

Table of Content

Sample Business Plan for Microfinance

Microfinance is a banking service that provides financial assistance to low-income individuals or groups who do not have access to formal financial services. In the US, microfinancing refers to loans of $50,000 or less. Microfinance institutions (MFIs) offer loans, savings, insurance, and other products to help clients improve their livelihoods, reduce their vulnerability, and achieve their goals.

This microfinance business plan template is about a sample microfinance bank that operates in the USA. It will provide an overview of a microfinance bank’s business models, services, customer focus, management team, success factors, financial highlights, and plans. Refer to our financial advisor business plan for a detailed understanding.

Executive Summary

Business Overview

InnoLoan is a microfinance bank that provides affordable and accessible financial services to low-income individuals and small businesses in the USA. Our mission is to empower our customers to improve their livelihoods, create jobs, and contribute to the economic development of their communities.

Services

InnoLoan microfinance bank offers a range of financial products and services to its clients, such as:

- Microloans – Tailored to the needs and capacities of our customers, with flexible repayment terms and competitive interest rates

- Savings products – Help our customers build assets and plan for the future

- Insurance products – Protect our customers from risks and uncertainties

- Money transfer – Enables our customers to send and receive money conveniently and securely

- Financial education program – Equips our customers with the skills and knowledge to manage their finances effectively

Customer Focus

Our target market comprises low-income individuals and small businesses excluded or underserved by the formal financial sector. We focus on women, youth, minorities, and rural populations facing multiple barriers to financial services. We segment our customers based on their demographic profile, income level, business activity, and financial needs.

Management Team

We have a strong management team with extensive experience and expertise in microfinance, banking, and social development. Our team is committed to delivering high-quality services to our customers and achieving social and financial impact. We also have a network of well-trained and motivated staff who work closely with our customers at the grassroots level.

Success Factors

Our success factors include:

- Clear vision and mission

- Customer-centric approach

- Diversified product portfolio

- Robust operational system

- Strong risk management framework

- Sound financial performance

- Positive social impact

Financial Highlights

Our financial highlights for the next five years are:

- Projected portfolio growth of 25% annually, reaching $50 million by 2026

- Projected customer base of 100,000 by 2026, with 60% women, 40% youth, 30% minorities, and 70% rural

- Projected revenue growth of 30% annually, reaching $15 million by 2026

- Projected net income growth of 35% annually, reaching $3 million by 2026

- Projected return on equity of 20% by 2026

- Projected operational self-sufficiency of 120% by 2026

Company Overview

Who is InnoLoan Microfinance Bank?

InnoLoan microfinance bank, established in 2020 in San Francisco, CA, is a US-registered and regulated bank that offers affordable and accessible financial services to low-income individuals and small businesses.

InnoLoan Micro Lending Company

InnoLoan micro-lending company, a branch of InnoLoan microfinance bank, gives small US businesses microloans from $500 to $10,000. It supports entrepreneurs with good business ideas or who need more capital.

Industry Analysis

The microfinance industry in the USA is a growing and dynamic sector that provides financial services to millions of low-income individuals and small businesses who are excluded or underserved by the formal financial sector.

According to the Global Microfinance Market Research Report 2023, the global Microfinance market reached USD 218.31 billion in 2022. The market is expected to achieve USD 447.76 billion by 2028, exhibiting a CAGR of 12.72% during the forecast period.

Here are some more interesting insights on the microfinance industry:

- There are approximately 10,000 microfinance institutions throughout the world. (Fit Small Business)

- Microfinance institutions worldwide serve more than 140 million borrowers and have a total loan portfolio estimated at $124 billion. (Microfinance Barometer Report)

Customer Analysis

Demographic Profile of Target Market

Our target market consists of low-income individuals and small businesses excluded or underserved by the formal financial sector in the USA. We estimate that over 50 million potential customers in this market segment need financial services but lack access to them. We focus on women, youth, minorities, and rural populations facing multiple barriers to financial services.

Customer Segmentation

We segment our customers based on their demographic profile, income level, business activity, and financial needs. The following table shows the characteristics and size of our customer segments:

| Customer Segment | Demographic Profile | Income Level | Business Activity | Market Size |

| Women | Female, aged 18-45 | Below $2,000 per month | Microenterprises | 20 million |

| Youth | Male or female, aged 15-24 | Below $1,000 per month | Start-ups or informal businesses | 15 million |

| Minorities | Ethnic or racial minorities | Below $1,500 per month | Small businesses | 10 million |

| Rural | Residents of rural areas or small towns | Below $1,500 per month | Small-scale farmers or agribusinesses | 5 million |

Competitive Analysis

Direct and Indirect Competitors

We face direct and indirect competition from various providers of financial services to low-income individuals and small businesses in the USA.

Some of the direct competitors include:

- MicroVest – A microfinance institution with over $50 million in loans to 100,000 customers. It gives microloans from $100 to $10,000 at 18% interest. It also provides 2% interest savings accounts and life and health insurance.

- MicroFlex – A microfinance institution with over $25 million in loans to 50,000 customers. It gives microloans from $50 to $5,000 at 15% interest. It also provides 1% interest savings accounts and a money transfer service with a 3% fee.

Some of the indirect competitors include:

- Payday lenders – Providers of short-term loans that charge high-interest rates and fees. They target customers who need urgent cash but have poor credit history or no collateral.

- Pawn shops – Providers of loans that require customers to pledge their personal belongings as collateral. They charge high-interest rates and fees and may sell the collateral if the customers fail to repay the loans.

- Credit unions – Non-profit financial cooperatives offering their members loans, savings, and other services. They charge lower interest rates and fees than other providers but have limited outreach and eligibility criteria.

Competitive Advantage

Our competitive advantage is based on the following factors:

- Clear vision and mission

- Customer-centric approach

- Diversified product portfolio

- Robust operational system

- Strong risk management framework

- Sound financial performance

- Positive social impact

Marketing Plan

Our marketing plan is designed to achieve the following objectives:

- To increase our brand awareness and recognition

- To attract new customers and retain existing ones

- To expand our market share and reach by entering new geographic areas

- To enhance our competitive position and reputation

Our marketing plan consists of the following strategies:

- Product strategy – We will continuously improve our products based on customer feedback and market research. We will also introduce new products in the future.

- Price strategy – We will offer competitive and affordable prices that reflect the value and quality of our services. We will also provide incentives and discounts for loyal customers and referrals.

- Place strategy – We will leverage our existing network of branches, agents, and partners to deliver our services to our customers.

- Promotion strategy – We will use traditional and digital media to communicate our value proposition and social impact to our target market and stakeholders.

Operations Plan

Operation Function

Our operations plan describes delivering customer services and managing our internal processes. Our operations plan consists of the following functions:

- Loan origination – We assess and approve microloan applicants using interviews, credit scores, collateral, and group lending, and assist them with the application process.

- Loan disbursement – We deliver the approved loan amount to our customers via cash, bank, mobile money, or prepaid cards, ensuring speed, ease, and safety.

- Loan collection – We collect the loan repayments from our customers as per agreement, using direct debit, mobile money, or cash collection, and monitor the loan performance and contact late customers to prevent defaults and losses.

- Savings mobilization – We offer and manage savings accounts for our customers who want to save money, with good interest rates and no minimum balance, and easy access and withdrawal options through branches, agents, mobile banking, or ATMs.

- Insurance provision – We offer insurance products that protect our customers from life, health, property, and business risks, working with good insurance companies to provide cheap and customized insurance plans, and handling the claims and payments for our customers in case of loss or damage.

- Money transfer service – We offer a money transfer service that allows our customers to send and receive money locally and internationally, working with reliable money transfer operators to provide fast and secure money transfer options, and charging low fees and offering good exchange rates.

- Financial education program – We run a financial education program for our customers who want to learn more, using workshops, seminars, online courses, or mobile apps, and measuring the impact of our program on customers’ financial behavior and well-being.

Milestones

- January 2024 – Launch of our microfinance bank with all the necessary licenses, registrations, and approvals

- June 2024 – Opening of 10 branches in strategic locations across California

- December 2024 – Reaching 10,000 customers with a loan portfolio of $5 million

- March 2025 – Introduction of new products such as insurance, money transfer, and financial education

- June 2025 – Expansion to new states

- December 2025 – Reaching 50,000 customers with a loan portfolio of $25 million

- March 2026 – Adoption of digital technologies such as mobile banking, online platforms, and biometric identification

- December 2026 – Reaching 100,000 customers with a loan portfolio of $50 million

Financial Plan

Our financial plan provides an overview of our key revenue and costs, funding requirements and use of funds, key assumptions, and financial projections. Refer to our bookkeeping business plan here.

Key Revenue & Costs

Our key revenue sources are:

- Interest income – The income generated from charging interest on our microloans. We charge an average interest rate of 16% per annum on our microloans.

- Fee income – The income generated from charging fees for our services. We charge an average fee of 2% per transaction on our services.

- Other income – The income generated from other sources such as grants, donations, investments, etc. We expect to receive an average of $500,000 annually from other sources.

Our key cost drivers are:

- Operating expenses – The expenses incurred for running our operations, such as salaries, rent, utilities, travel, marketing, etc. Our operating expenses will be 40% of our total revenue.

- Loan loss provision – The provision made for potential losses due to loan default or delinquency. We estimate that our loan loss provision will be 5% of our total loan portfolio.

- Capital expenditure – The expenditure for acquiring or upgrading fixed assets such as equipment, software, vehicles, etc. Our capital expenditure will be 10% of our total revenue.

Funding Requirements and Use of Funds

We require a total funding of $10 million to launch and grow our microfinance bank in the next five years. We plan to raise this funding from various sources such as equity, debt, grants, etc. The following table shows the breakdown of our funding sources and amounts:

| Funding Source | Amount | Percentage |

| Equity | $4 million | 40% |

| Debt | $4 million | 40% |

| Grants | $2 million | 20% |

Key Assumptions

Our financial plan is based on the following key assumptions:

- Market share – We will capture 0.2% of our target market by 2026 (100,000 customers)

- Portfolio growth – Our loan portfolio will grow at an annual rate of 25% ($50 million by 2026)

- Revenue growth – Our revenue will grow at an annual rate of 30% ($15 million by 2026)

- Net income growth – Our net income will grow at an annual rate of 35% ($3 million by 2026)

- Return on equity – Our return on equity will be 20% by 2026

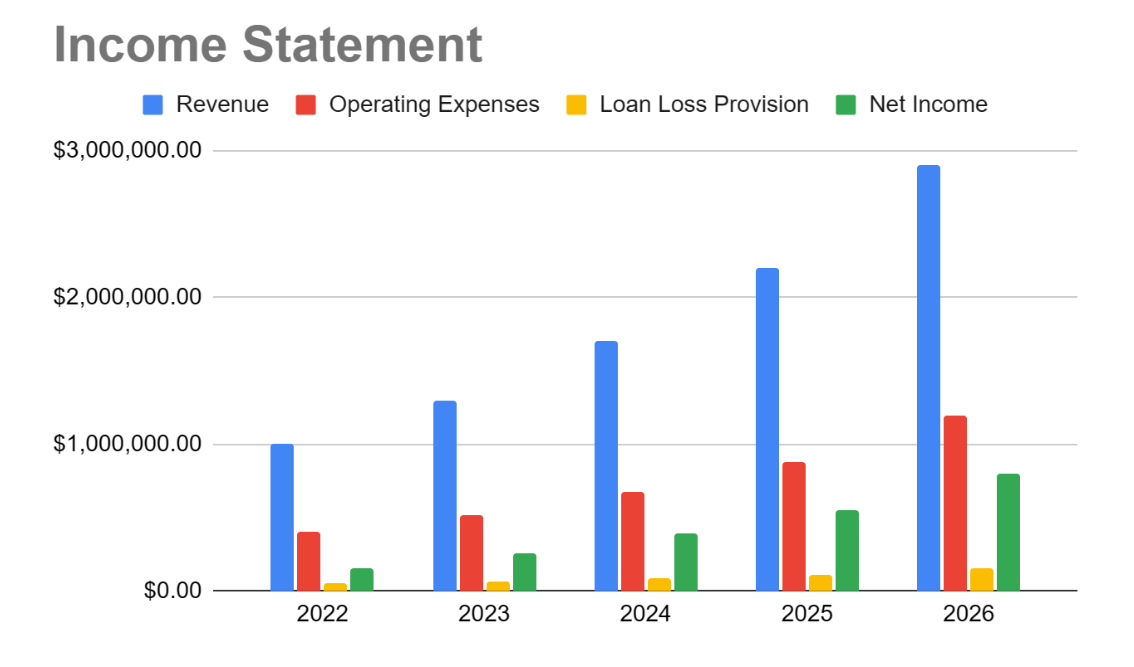

Income Statement

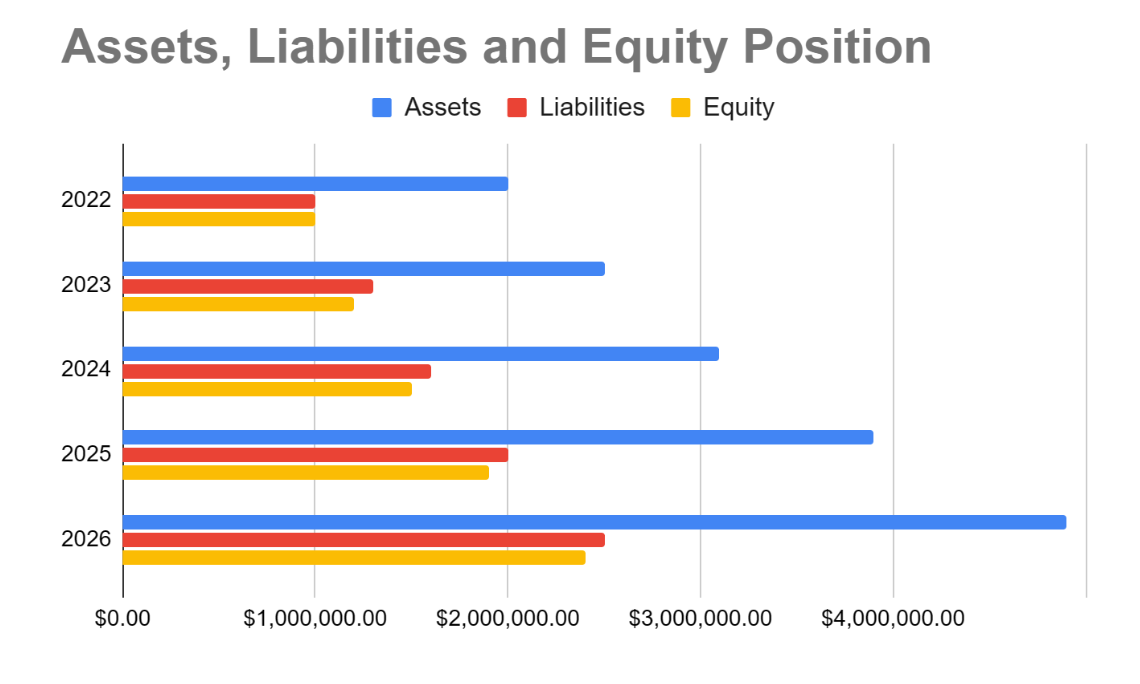

Balance Sheet

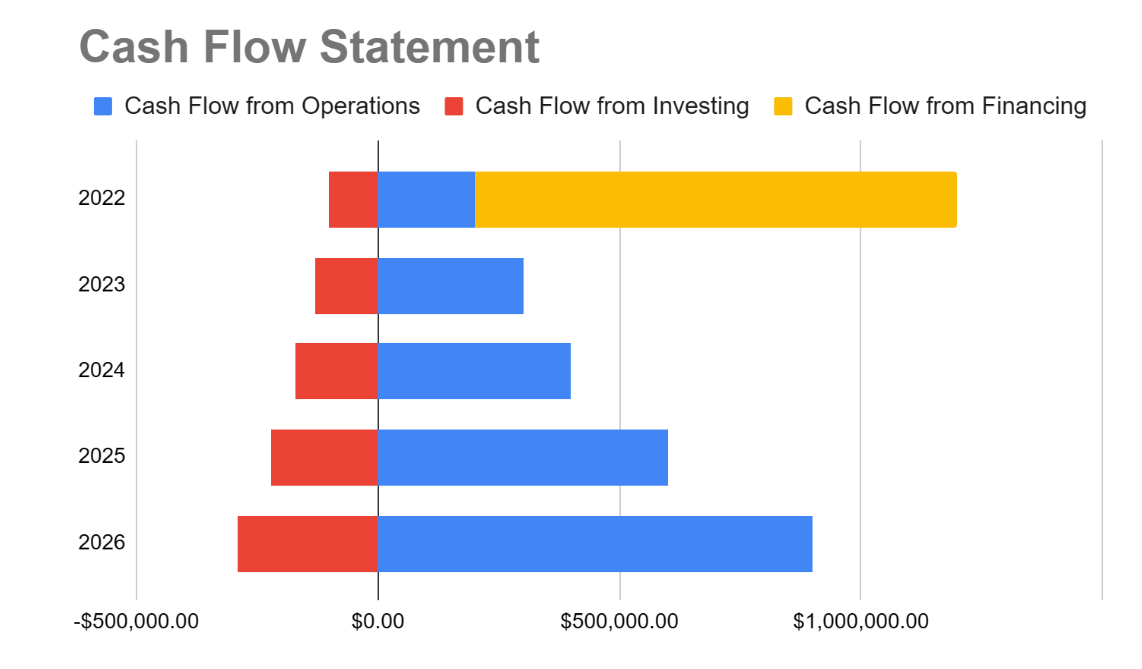

Cash Flow Statement

Hire OGSCapital for Your Microfinance Business Plan

Writing a microfinance business plan is hard and time-consuming. That’s why you should hire us, OGSCapital. We are a team of leading business plan experts, having helped over 5,000 clients attract over $2.7 billion in financing and achieve their business goals. We have a team of experienced and qualified business plan experts and SBA business plan consultants who have worked in various industries and sectors, including microfinance. We know how to create a compelling and customized five-year microfinance business plan that will meet the expectations of your target audience.

We will also provide strategic advice, market research, financial projections, and graphic design to make your micro loan business plan stand out. Contact us for a free consultation and quote for your microfinance business plan template.

Frequently Asked Questions

How much capital is required to start a microfinance company?

In the US, you may need a minimum capital of $5 million to register as a non-banking financial company (NBFC) microfinance institution. You should have a microfinance institution business plan showing your projected income and expenses for the next five years, or refer to our loan officer business plan.

Is the microfinance business profitable?

Microfinance business can be profitable in the US if you deliver high-quality services that meet the needs and preferences of your target market. You can also use digital technologies or a payday loan business plan to manage costs and risks and show your social and financial impact.

How do I start a microfinance business?

To start a microfinance business, you must identify your target market, choose a specialty of finance, create a business plan, and comply with state and federal regulations. You also need a strategic business plan for a microfinance bank that outlines your vision, mission, goals, and strategies.

OGSCapital’s team has assisted thousands of entrepreneurs with top-rate business plan development, consultancy and analysis. They’ve helped thousands of SME owners secure more than $1.5 billion in funding, and they can do the same for you.